Dass dies bei einem Referenzzinssatz der SNB von 0,50% tatsächlich erlaubt ist, ist ein Raubüberfall. Es betrifft mich nicht, ich bezahle meine Kreditkarten (die ich nur in der Schweiz verwende) jeden Monat vollständig. Vielleicht ist es an der Zeit, darüber zu diskutieren, welche Karten wo verwendet werden sollen (Debit/Kredit in der Schweiz und im Ausland).

Die Antwort ist einfach: Verwenden Sie eine Postpaid-Karte wie diese Cashback- und Swisscard-Karten nur in der Schweiz. Bei Devisen wird eine Marge von 2,5 % über dem Referenzkurs erhoben (um die Sache noch komplizierter zu machen, handelt es sich hierbei möglicherweise nicht um den Interbankkurs, sondern um einen „internen“ Swisscard-Kurs.

Verwenden Sie im Ausland eine Debitkarte, im Ausland eine Prepaid-Kreditkarte (Neon, Wise, Revolut). Die Margen für Devisen betragen einen Bruchteil der Kosten der oben genannten Kreditkarten.

Kassensturz hat dazu im September etwas beigetragen (auf Deutsch): https://www.srf.ch/sendungen/kassensturz-espresso/tests/kostenvergleich-debit-und-kreditkarten-im-test-sparen-beim-zahlen

https://i.redd.it/vu8btmqu1s7e1.jpeg

Von emptyquant

12 Comments

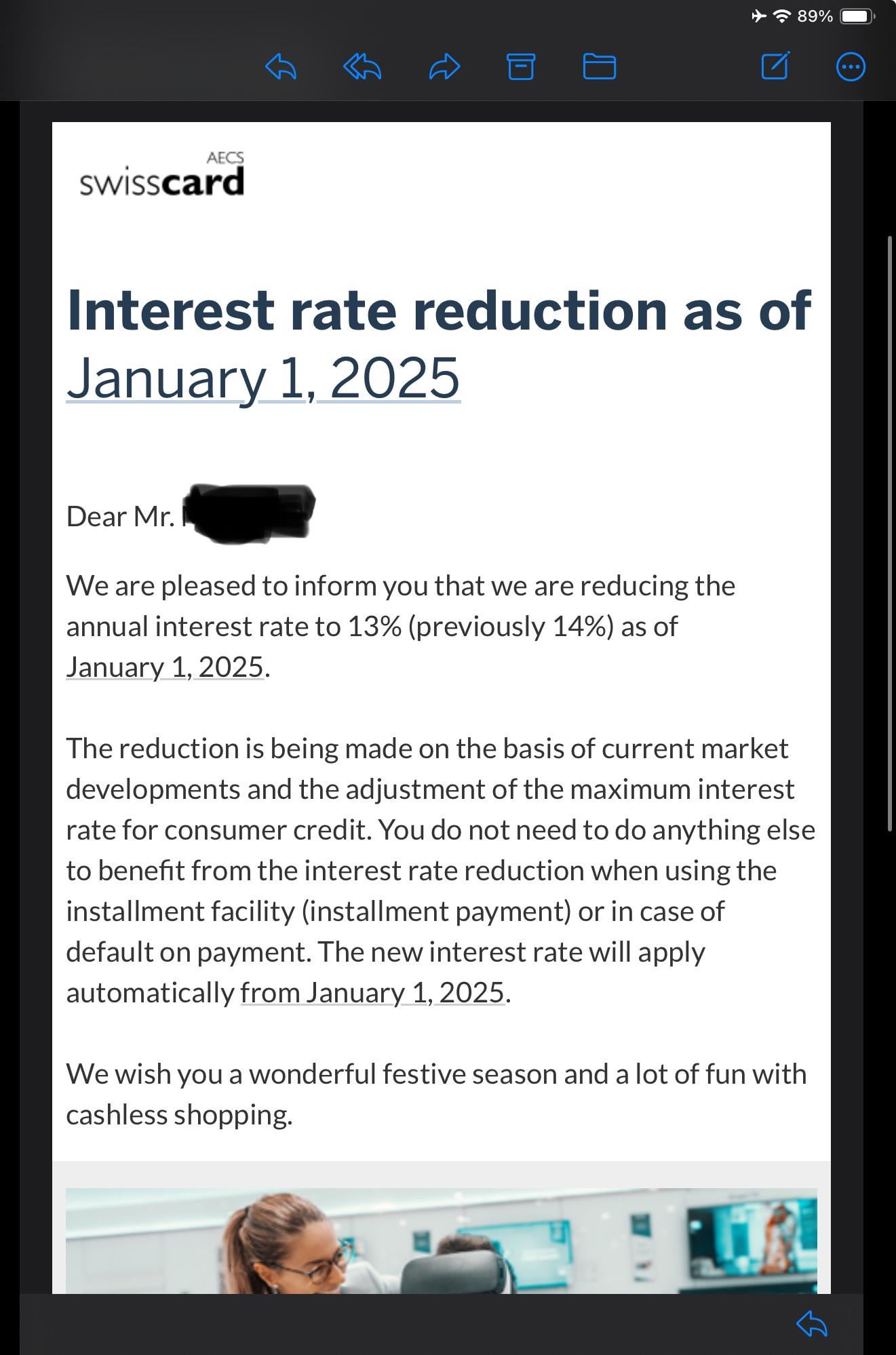

14% wow…

when i used them i think it was at 12% which is already high i think it’s time to boycott them.

OP do you understand what a risk premium is?

That interest is for if you go beyond (!) the agreed upon loan (i.e. don’t pay it off after a month) and include punishment fees obviously. You can‘t compare that to the SNB interest rate which influences savings interest and mortgage. Which is also an agreed upon amount.

US credit cards charge on average 29% and people actually acquire a lot of debt on them compared to us. 13% for a credit card that shouldn’t really be used as a line of credit for more than a couple days, maybe a month in an emergency seems pretty reasonable actually.

Who actually doesn’t pay their credit card bill monthly?

One who uses a credit card not just as a means of payment but actually for credit has lost control of their life.

If you can’t pay off your credit card debt within 1 month you shouldn’t have a credit card. There are way too many people in debt nowadays. Interest rates obviously only affect those who don’t pay back the full amount they spent.

Unpopular Opinion: I don’t think you should have a credit card if you are planning or too often paying the interest fees.

So what? The average Swiss credit card holder uses it as payment tool, not as credit vehicle. Regular payoff at the end of a cycle and the issuer can ask for any annual interest, it doesn’t matter.

Considering it is set by law, it is actually ok. Alternatively they could have raised it to 29.9% during the last years, just like the American providers….but yeah, I’m with you …1% is total BS

Daylight robbery is what happens in the USA. I think there is no cap on the interest rate a credit card issuer can charge.

What is good about their credit cards? They just feel worse and more useless than viseca. Or am I totally off the mark?